Share

-

-

COPIED

Welcome back to the Now Newsletter. I’m Matt Medved.

It’s tax week in America — that special season when every questionable decision made during the bull run comes back to haunt you. Just ask one Pennsylvania man who failed to report $13 million in CryptoPunks profits. He just pled guilty this week, joining an exclusive club no one wants to be part of: NFT whales turned federal defendants.

The lesson? The IRS may not know the difference between a zombie Punk and an ape—but they definitely know what capital gains look like.

Chances are, your week went better than his. Unless, of course, you held Mantra. Mantra’s OM token nosedived 90% after $227M worth was dumped onto exchanges by 17 wallets — sparking liquidation cascades and insider rumors. CEO JP Mullin took to CoffeeZilla to do damage control — and delivered the cringiest performance since Hayden Davis tried to spin Libra.

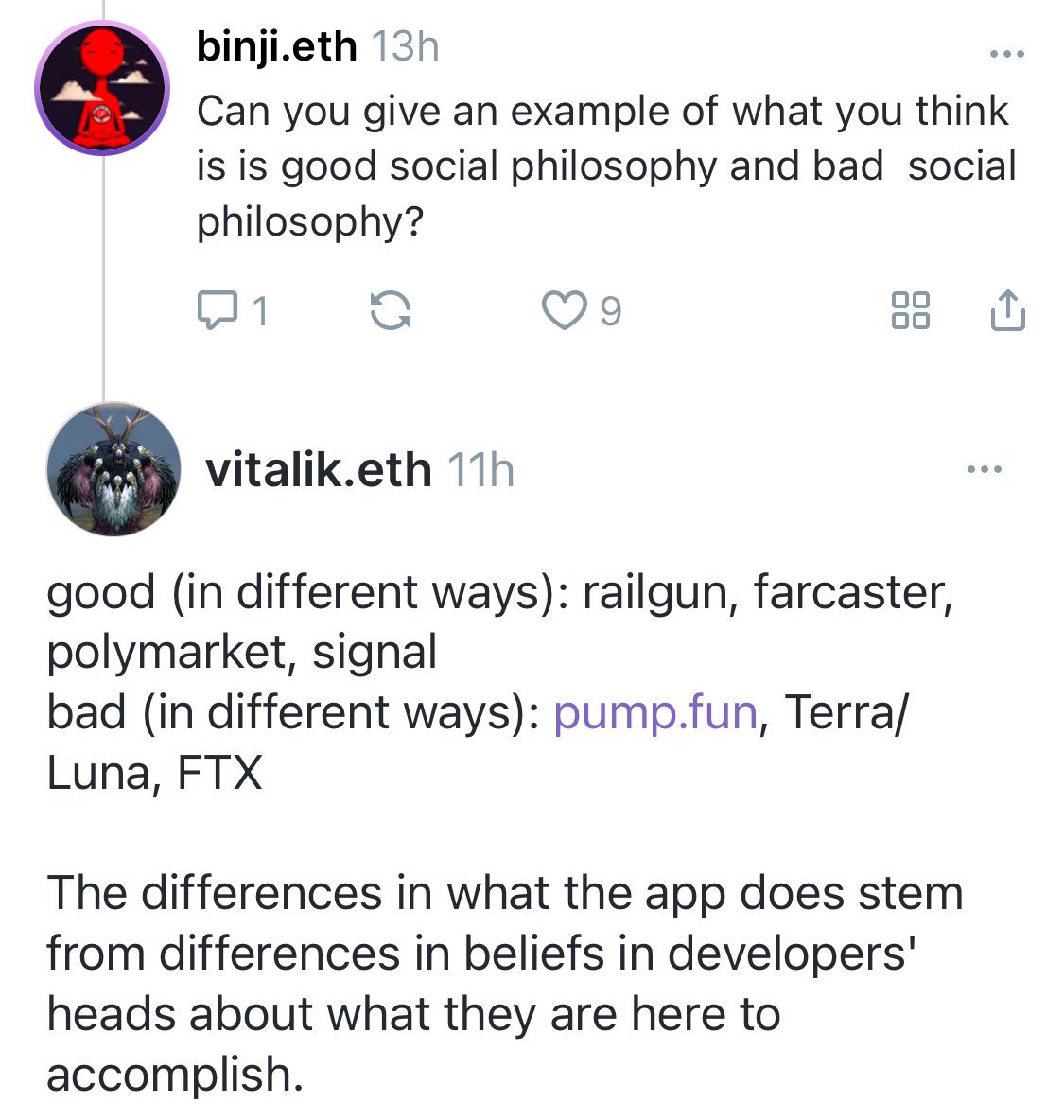

And then there’s Pump.fun — the viral launchpad at the center of crypto’s latest culture war. Vitalik compared it to FTX and Terra, setting off a firestorm between Ethereum purists and Solana shitcoiners. Here are my thoughts.

The Pump.Fun Debate

Is Pump.fun bad for the crypto space?

It’s a question that echoed through last year’s memecoin mania. But this week, the Solana token launchpad is in the spotlight — sparked by controversial comments from Ethereum co-founder Vitalik Buterin.

In a reply on Farcaster, Buterin grouped Pump.fun with the dreaded likes of Terra/Luna and FTX — citing them as examples of “bad social philosophy.” Crypto Twitter didn’t hold back. Solana co-founder Anatoly Yakovenko shot back, “When you don’t have PMF, you have politics.” Nick “Choose Rich” O’Neill added, “If you think Pump.fun is bad for crypto, you are stupid.”

Critics were quick to counter that Pump.fun’s success is a net negative for the ecosystem due to its extractive nature. Investor/commentator Beanie decried it as “likely the biggest and most extractive scam in crypto history.” Some have blamed it for the absence of a traditional “alt season” this cycle, as capital fled majors for illiquid memecoins — leaving most retail traders holding the bag.

I’ve spent more than a few questionable late nights chasing the mirage of generational wealth in the memecoin trenches. Hunter S. Thompson once called the music industry “a cruel and shallow money trench… a long plastic hallway where thieves and pimps run free, and good men die like dogs.” After nearly a decade at Billboard and Spin, I can tell you: that circus doesn’t hold a candle to crypto’s unhinged casino.

For the uninitiated, Pump.fun is a viral Solana launchpad that turned memecoin creation into a frictionless game. Anyone could instantly mint a token — no coding, no liquidity — thanks to an auto-pricing bonding curve. For a moment, it felt like crypto’s fairest arena: no VCs, no insider rounds, just a wallet, an idea, and a shot at virality.

But the reality was messier. Bots and snipers front-ran launches, scams and rug pulls were rampant, and most tokens collapsed quickly. More than 98% of launches never graduate beyond Pump.fun, turning the promise of fair finance into a high-speed onchain casino where the odds were stacked from the start.

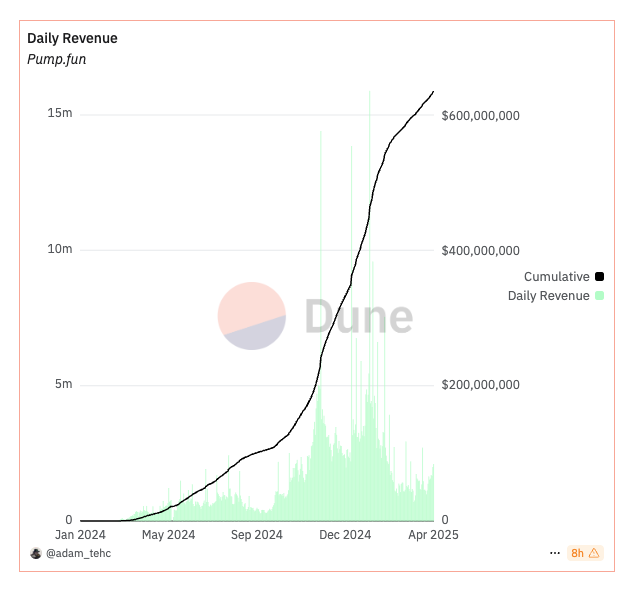

By any traditional metric, Pump.fun is a breakout success. Since launching in 2024, it has racked up over $612 million in fees — proof that it’s achieved the elusive product-market fit. Despite the recent market downturn, the platform still averaged more than $100 million in daily volume over the past two weeks.

Its now-retired livestreaming feature, shut down amid concerns over self-harm and abuse, made such a cultural splash that it even inspired a dystopian new episode of “Black Mirror.”

Pump.fun didn’t rise in a vacuum — it arguably filled one. With Gary Gensler and the previous administration’s SEC choking off traditional paths to fair token launches, builders got creative. It’s not the system anyone asked for, but when the rules are unclear or actively hostile, people invent their own games. When legitimacy is off-limits, attention becomes the only moat that matters.

The debate lays bare a harsh truth: in crypto, speculation isn’t a byproduct — it’s the product. And gambling remains its most proven product-market fit.

The truth is, speculation’s always been crypto’s most reliable growth engine. ICOs bankrolled major blockchains. DeFi Summer dressed up ponzinomics as protocol design. NFTs brought in creators and mainstream culture. Memecoins ditched the whitepapers and empty promises and gave the degens exactly what they wanted. Every cycle looked like a joke — right up until it didn’t.

The genie is not going back inside the bottle. Pump.fun is moving to vertically integrate its business with the launch of PumpSwap, its native DEX which processed $2.5 billion worth of trades last week. It has spawned countless clones, as well as legitimate competing businesses like MoonShot. Just today, Raydium announced its LaunchLab competitor to Pump.Fun. In this market, even a sliver of Pump.fun’s volume is enough to power a viable web3 business.

The gambling craze isn’t unique to crypto — it’s a broader cultural shift. Sports betting is booming, with U.S. sportsbooks posting a record $13.71 billion in revenue in 2024. Online gambling is projected to top $250 billion globally by 2034. Prediction markets like Polymarket are surging too, turning elections, court cases, and celebrity drama into tradable assets.

Pump.fun didn’t break crypto — it exposed it. Strip away the narratives, and what’s left is the raw market instinct: gamble first, ask questions later. It may not be the future we envisioned, but it’s the one we built. And as long as speculation outpaces substance, the casino will keep printing — whether it’s good for us or not.

Subscribe to our free weekly newsletter here.